As published in print with

Since 1986, when President Yoweri Museveni was first elected, Uganda’s GDP has multiplied by a factor of six. Today, with economic growth all but guaranteed thanks to the imminent start of oil production, the government is now working on economic transformation

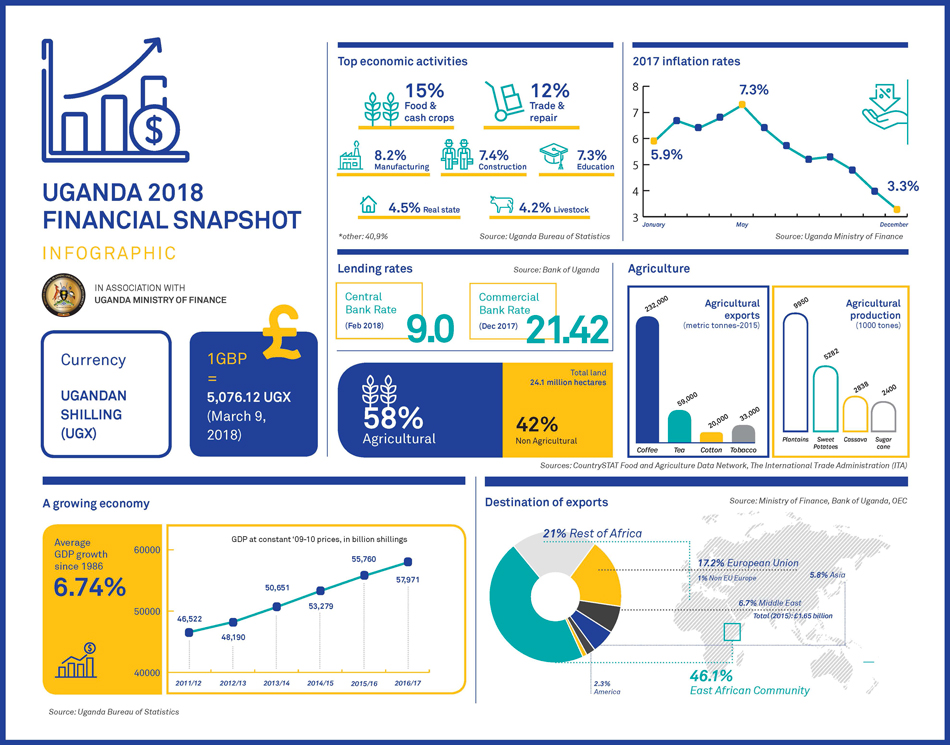

Uganda’s economy has grown consistently since the end of the armed conflict in 1986, when a number of structural reforms and investments brought about an annual average of seven per cent GDP growth during the 1990s and early 2000s. This, however, slowed to 4.5 per cent in the five years to 2015/16, and to 3.9 per cent last year amid the aftereffects of global financial crisis, the downturn in commodity prices and, starting in 2013, the civil war in major export partner South Sudan. Today, officials are optimistic that this slowdown is only temporary, with central bank governor Emmanuel Tumusiime-Mutebile forecasting a rebound in real GDP growth to five per cent in the 2017/18 financial year.

A key driver of future growth will be the bringing on stream of the large oil reserves first discovered in the country in 2006. But this process must be carefully managed. “Our greatest challenge on the horizon will be to maintain macroeconomic stability once Uganda begins to produce oil in commercial quantities, which is expected in the early 2020s,” says Mr Tumusiime-Mutebile. “The production of oil often destabilises the macro-economy because of domestic spending booms and exchange rate volatility. However, I am confident that the Bank of Uganda has the requisite monetary policy tools and the commitment needed to manage this challenge.”

The government plans to consolidate growth over the long term in a range of ways through its current National Development Plan (NDPII) – the second in a series of six five-year programmes aimed at achieving Vision 2040. Its objective is to propel the country towards middle-income status by 2020 by strengthening competitiveness for sustainable wealth creation, employment and inclusive growth.

Modernising the agricultural sector, which employs the majority of Ugandans, is a top priority. Operation Wealth Creation, implemented by the Uganda Peoples Defence Forces, is currently supplying farmers in different regions of the country with inputs from seeds to fertiliser to improve incomes and productivity.

Work is also underway to improve access to credit. This is already paying off: in 2009, 30 per cent of the population were excluded from all types of financial services, whereas by 2013 this figure had fallen to 15 per cent, says Mr Tumusiime-Mutebile. A new five-year financial inclusion strategy, launched in 2017, seeks to further strengthen credit infrastructure, especially for MSMEs, and build a digital infrastructure for financial services, all of which will enable the country’s private sector to become an engine for stable economic growth.